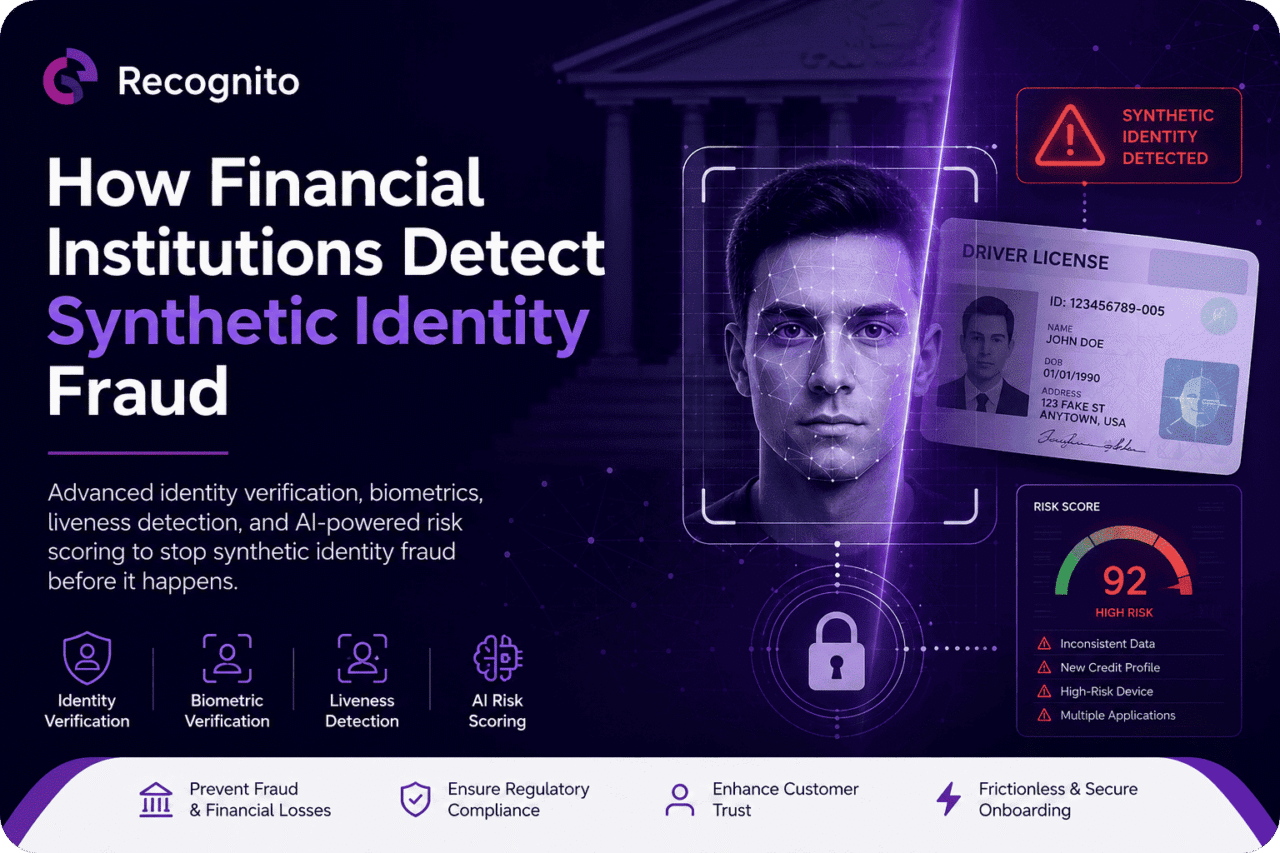

Synthetic identity fraud has emerged as one of the most damaging forms of financial crime facing banks, fintech companies, lenders, and digital payment providers. Unlike traditional identity theft, where criminals steal a real person’s information, synthetic identity fraud involves creating an entirely new identity by combining genuine and fabricated data.

A fraudster may use a legitimate Social Security Number, passport number, or government-issued identifier alongside a fake name, email address, phone number, and residential address. The resulting synthetic identity often appears legitimate enough to pass basic onboarding checks, making it difficult for organizations to identify fraudulent applicants before financial losses occur.

As financial institutions accelerate digital transformation and remote onboarding, advanced identity verification and biometric verification technologies have become critical tools in modern fraud prevention strategies.

What Is Synthetic Identity Fraud?

Synthetic identity fraud occurs when criminals create a false identity using a mixture of real and fabricated information.

Unlike traditional identity theft, the fraudster is not impersonating an existing individual. Instead, they create a new identity that does not belong to anyone but appears authentic to verification systems.

Synthetic identities are commonly used to:

- Open bank accounts

- Obtain loans and credit cards

- Bypass KYC requirements

- Commit account fraud

- Launder money

- Circumvent onboarding controls

These identities often remain active for months or years before being used for large-scale fraud, making identity fraud detection particularly challenging.

According to the Federal Trade Commission, identity-related fraud continues to increase as cybercriminals gain access to larger volumes of personal information through data breaches and online attacks.

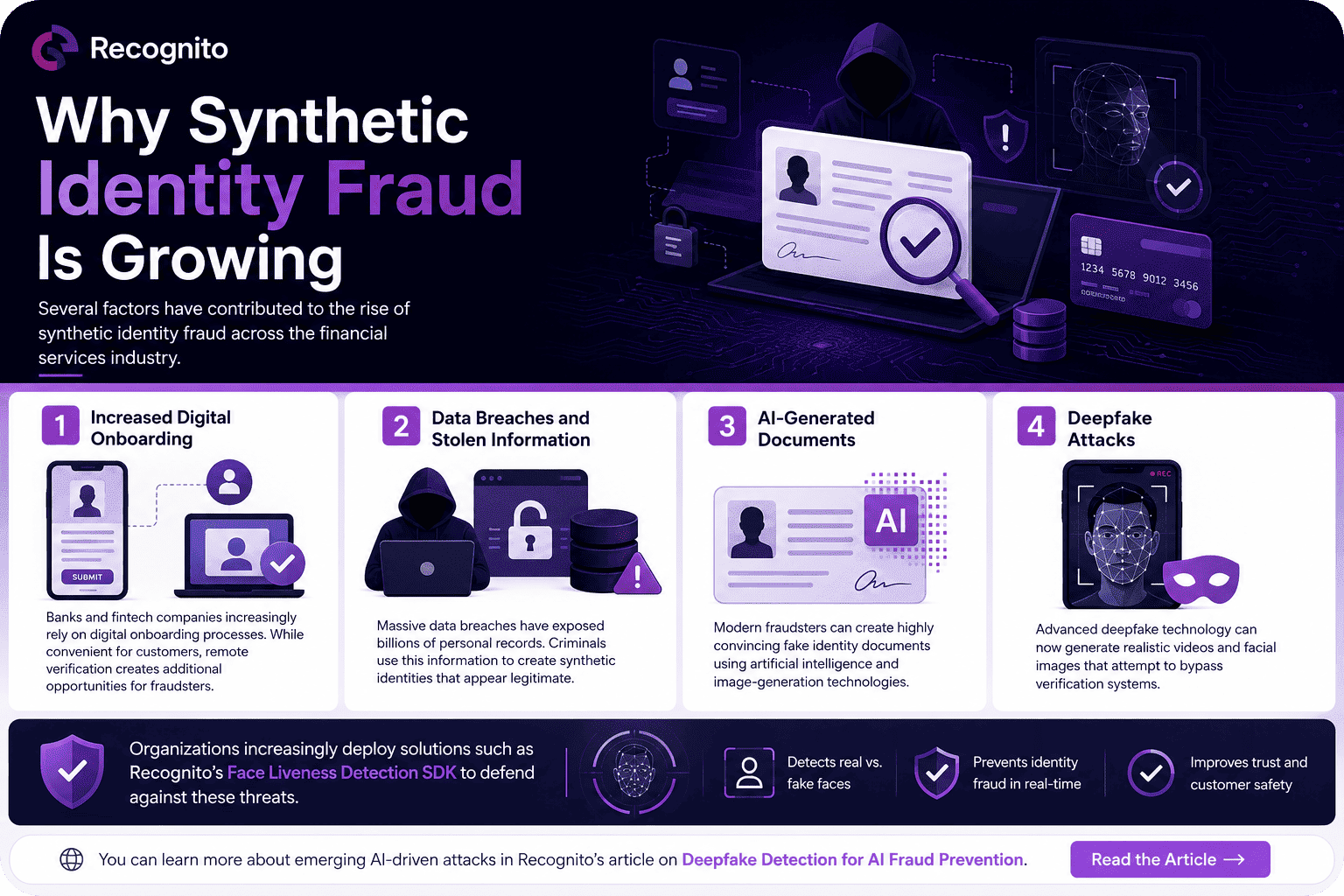

Why Synthetic Identity Fraud Is Growing

Several factors have contributed to the rise of synthetic identity fraud across the financial services industry.

1. Increased Digital Onboarding

Banks and fintech companies increasingly rely on digital onboarding processes. While convenient for customers, remote verification creates additional opportunities for fraudsters.

2. Data Breaches and Stolen Information

Massive data breaches have exposed billions of personal records. Criminals use this information to create synthetic identities that appear legitimate.

3. AI-Generated Documents

Modern fraudsters can create highly convincing fake identity documents using artificial intelligence and image-generation technologies.

4. Deepfake Attacks

Advanced deepfake technology can now generate realistic videos and facial images that attempt to bypass verification systems. Organizations increasingly deploy solutions such as Recognito’s Face Liveness Detection SDK to defend against these threats.

You can learn more about emerging AI-driven attacks in Recognito’s article on Deepfake Detection for AI Fraud Prevention.

Why Traditional Fraud Prevention Methods Fail

Traditional fraud prevention approaches were not designed to handle modern synthetic identities.

Historically, institutions relied on:

- Knowledge-based authentication

- Passwords

- Security questions

- Manual document reviews

- Credit history checks

The problem is that much of this information can now be obtained from compromised databases or purchased on criminal marketplaces.

As a result, financial institutions must adopt a layered identity verification strategy rather than relying on a single verification method.

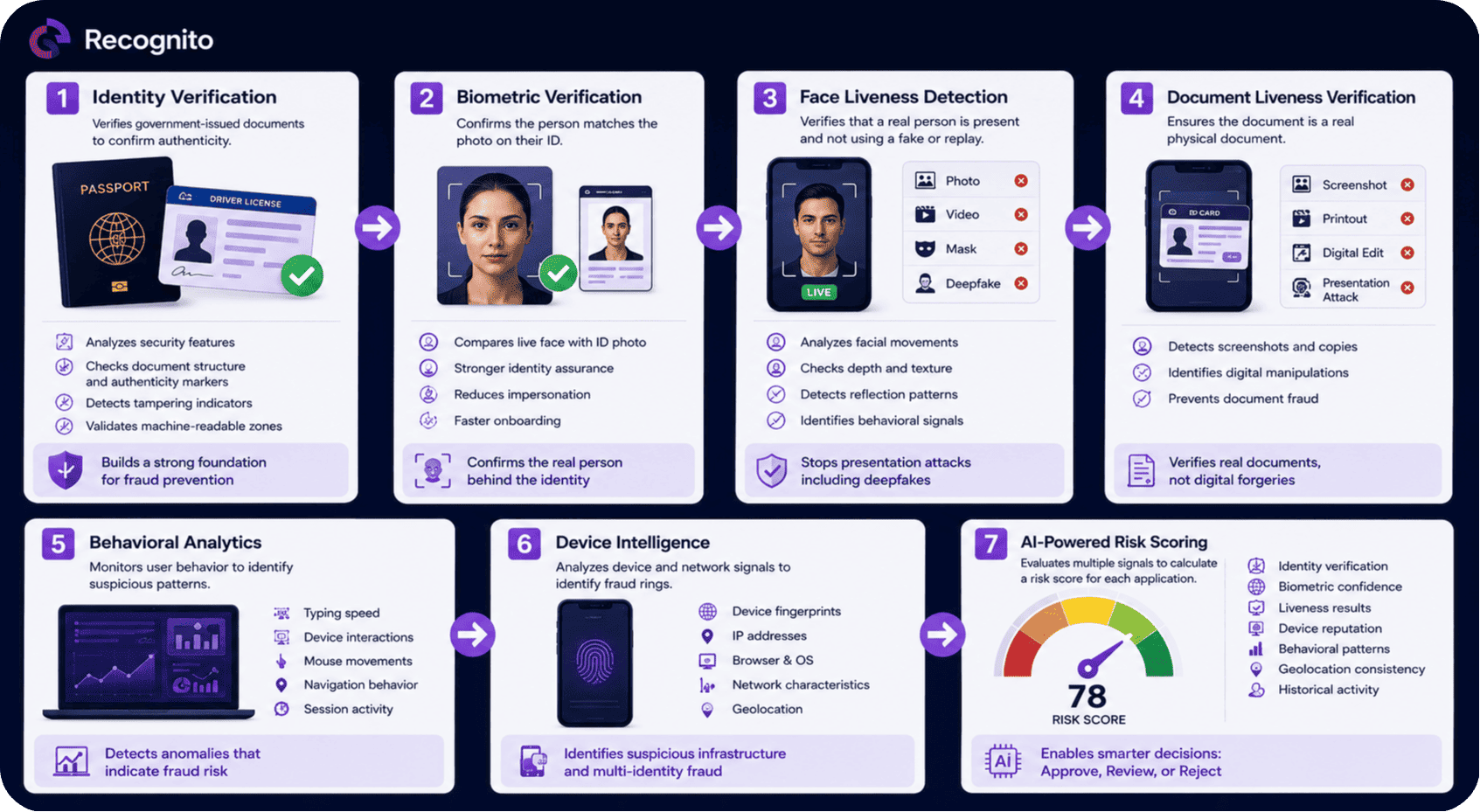

How Financial Institutions Detect Synthetic Identity Fraud

Modern financial institutions use multiple technologies working together to identify fraudulent applicants and prevent account creation.

1. Identity Verification

Identity verification serves as the foundation of synthetic identity fraud prevention.

During onboarding, organizations verify government-issued documents such as:

- Passports

- National ID cards

- Driver’s licenses

- Residence permits

Modern document verification systems analyze:

- Security features

- Machine-readable zones

- Document structure

- Typography

- Tampering indicators

- Authenticity markers

Organizations using solutions like Recognito’s ID Document Recognition SDK can automate document verification while reducing manual review requirements.

Strong identity verification processes also help organizations comply with regulations such as the General Data Protection Regulation (GDPR).

2. Biometric Verification

A valid document does not necessarily prove that the individual presenting it is the rightful owner.

Biometric verification helps solve this challenge by comparing a live facial image against the photo contained within an identity document.

Benefits of biometric verification include:

- Stronger identity assurance

- Reduced impersonation attempts

- Faster onboarding processes

- Improved fraud prevention

- Better customer experience

Financial institutions increasingly implement advanced facial recognition technologies such as Recognito’s Face Recognition SDK to strengthen onboarding security.

Independent testing programs such as the NIST Face Recognition Vendor Test (FRVT) continue to demonstrate significant improvements in biometric accuracy.

3. Face Liveness Detection

One of the biggest weaknesses in traditional biometric systems is their susceptibility to presentation attacks.

Fraudsters may attempt to use:

- Printed photographs

- Mobile phone screens

- Video replays

- Deepfake videos

- 3D masks

Face liveness detection verifies that a real person is physically present during the verification process.

Advanced liveness detection systems analyze:

- Facial movement

- Depth information

- Reflection patterns

- Texture analysis

- Behavioral signals

Organizations implementing Recognito’s Face Liveness Detection SDK can significantly reduce fraud attempts involving synthetic identities and deepfakes.

For a deeper understanding of liveness verification, see Recognito’s article on How Face Recognition Liveness Detection Works.

4. Document Liveness Verification

Fraudsters frequently submit screenshots, photocopies, or digitally manipulated documents during onboarding.

Document liveness verification helps determine whether an actual physical document is present.

This technology can identify:

- Screenshots

- Printed reproductions

- Digital manipulations

- Document presentation attacks

Financial institutions increasingly deploy solutions such as Recognito’s ID Document Liveness Detection SDK to strengthen fraud prevention controls.

Organizations looking to improve onboarding security can also review Recognito’s article on Why Document Liveness Detection Is Essential for KYC Verification.

5. Behavioral Analytics

Even when identity documents and biometrics appear legitimate, fraudsters often exhibit suspicious behavior patterns.

Behavioral analytics monitors signals such as:

- Typing speed

- Device interactions

- Mouse movements

- Navigation behavior

- Session activity

Machine learning models identify anomalies that may indicate synthetic identity fraud.

This provides an additional layer of identity fraud detection beyond document and biometric verification.

6. Device Intelligence

Device intelligence helps identify fraud rings operating multiple synthetic identities.

Financial institutions analyze:

- Device fingerprints

- Browser configurations

- Operating systems

- IP addresses

- Network characteristics

- Geolocation information

When multiple applications originate from suspicious infrastructure, fraud prevention systems can trigger additional verification checks.

7. AI-Powered Risk Scoring

Modern fraud prevention systems use artificial intelligence to evaluate hundreds of signals simultaneously.

Risk engines analyze:

- Identity verification results

- Biometric verification confidence

- Liveness detection outcomes

- Device reputation

- Behavioral patterns

- Historical activity

- Geolocation consistency

Each application receives a risk score that helps determine whether the customer should be approved, rejected, or manually reviewed.

This approach allows financial institutions to improve fraud prevention without increasing onboarding friction.

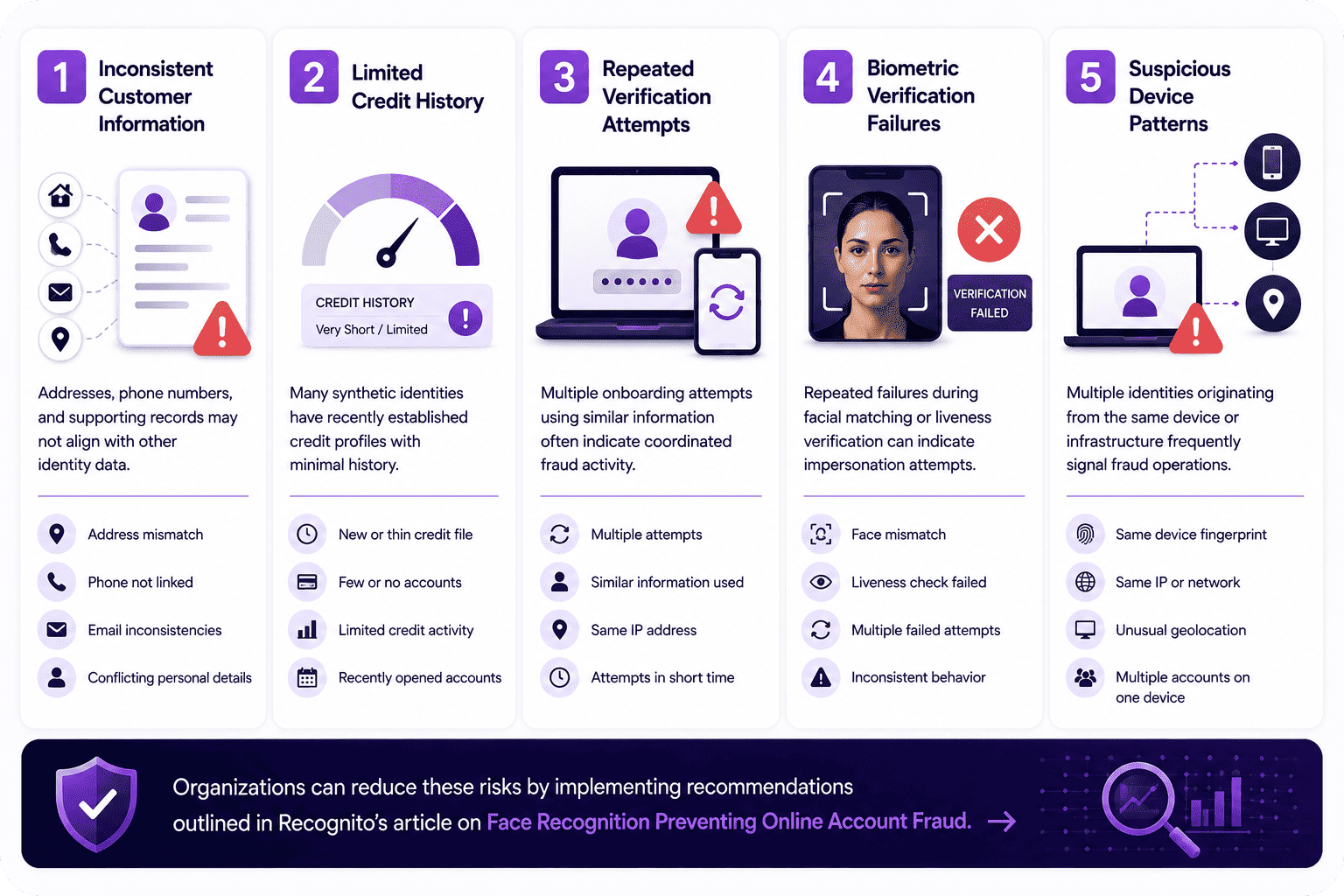

Common Red Flags Associated With Synthetic Identity Fraud

Financial institutions continuously monitor for warning signs that may indicate synthetic identities.

Some of the most common indicators include:

1. Inconsistent Customer Information

Addresses, phone numbers, and supporting records may not align with other identity data.

2. Limited Credit History

Many synthetic identities have recently established credit profiles with minimal history.

3. Repeated Verification Attempts

Multiple onboarding attempts using similar information often indicate coordinated fraud activity.

4. Biometric Verification Failures

Repeated failures during facial matching or liveness verification can indicate impersonation attempts.

5. Suspicious Device Patterns

Multiple identities originating from the same device or infrastructure frequently signal fraud operations.

Organizations can reduce these risks by implementing recommendations outlined in Recognito’s article on Face Recognition Preventing Online Account Fraud.

Building a Modern Fraud Prevention Framework

The most successful financial institutions use a layered fraud prevention strategy.

A modern framework typically includes:

- Identity verification

- Biometric verification

- Face liveness detection

- Document liveness verification

- Behavioral analytics

- Device intelligence

- AI-powered risk scoring

Combining these technologies significantly improves fraud detection while maintaining a smooth customer experience.

Organizations can further strengthen their verification programs by following guidance published by the Financial Action Task Force (FATF).

For development teams evaluating implementation options, the official Recognito GitHub repository provides additional technical resources and SDK information.

The Future of Synthetic Identity Fraud Detection

Synthetic identity fraud will continue to evolve as fraudsters gain access to increasingly sophisticated technologies.

Financial institutions are responding by investing in:

- Passive liveness detection

- Continuous identity verification

- Behavioral biometrics

- Real-time fraud intelligence

- Deepfake detection systems

- AI-powered risk orchestration

Research initiatives such as the NIST FRVT evaluations continue to improve the accuracy and effectiveness of biometric verification technologies across the industry.

Organizations that adopt advanced verification technologies today will be better positioned to prevent future fraud threats.

Conclusion

Synthetic identity fraud has become one of the most significant threats facing modern financial institutions. Traditional verification methods alone can no longer keep pace with increasingly sophisticated fraud techniques.

To effectively combat synthetic identities, organizations must implement a layered fraud prevention strategy that combines identity verification, biometric verification, face liveness detection, document liveness verification, behavioral analytics, device intelligence, and AI-powered risk scoring.

By adopting advanced verification technologies such as Recognito’s identity and biometric verification solutions, financial institutions can reduce fraud risk, improve compliance, and create a more secure onboarding experience for legitimate customers.

Frequently Asked Questions

What is synthetic identity fraud?

Synthetic identity fraud occurs when criminals create a new identity using a combination of real and fabricated information to deceive verification systems.

How do financial institutions detect synthetic identity fraud?

Financial institutions use identity verification, biometric verification, face liveness detection, document authentication, behavioral analytics, device intelligence, and AI-powered fraud prevention systems.

Why is biometric verification important for fraud prevention?

Biometric verification helps confirm that the person presenting an identity document is its legitimate owner, reducing impersonation and identity fraud risks.

Can synthetic identities pass traditional KYC checks?

Yes. Many synthetic identities are specifically designed to pass basic KYC and onboarding checks, which is why advanced verification technologies are increasingly necessary.

How does face liveness detection help prevent synthetic identity fraud?

Face liveness detection verifies that a real person is physically present during onboarding and helps prevent attacks involving photographs, video replays, masks, and deepfakes.